Equitable, and not very costly to government, if at all

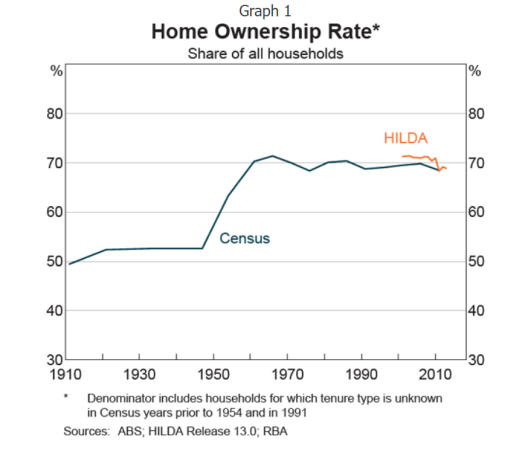

The ability for individuals to deduct current investment losses against current income, often inaccurately referred to as “negative gearing”, is at risk again as the federal government, at the urging of various interests, toys with the idea of abolishing it. Property investments are often negatively geared because the return on residential real estate is extraordinarily low, so investors resort to financial engineering to leverage a decent return on their capital. The average house in Sydney is now approximately $1.4 million while the average housing rental is 54,072 per annum. This is a gross return, before tax, management fees, maintenance, rates and land tax of only 3.9%. A bank deposits would return more. However, gearing the property so that the owner’s equity is much smaller than the total value of the property can magnify even a 2% annual increase in property value to 8% on equitywith a 25% deposit, or 10% with a 20% deposit. The arguments against “negative gearing” are conceptually wrong, even in the cases where there is some mathematical modelling to support the proposition. We have listed the most prominent conceptual mistakes here, and I hope after reading them you use this information to interrogate the claims for “negative gearing” opponents. Negative gearing is a tax dodge It is not a dodge, it is a necessary feature of an equitable tax system, and it has been available since before Commonwealth personal income tax was established. If you are to group someone’s sources of income together and tax the profits from their investments at their highest marginal rate, which is what we do, what is inequitable about allowing them a deduction at their highest marginal rate when those investments are losing money? To do anything else would be inconsistent, and unjust. The investor receives a tax return not as a concession from the government, but because they have been paying tax assessed in an income which is higher than the one they have actually earned. The whole of the deduction is very “costly” to the government Most proposals to abolish negative gearing benefits allow expenses to be carried forward against the future income from the investment. If losses are carried forward it means that the future profits are reduced by those losses, so the investor gets much the same benefit, just with a time lag. The “cost” to government is the interest on the deductions over the period, which is much less than the whole deduction, and a fraction of the “cost” calculated by many economists and think tanks. Most models do not factor this in, and this “cost” is even lower when you consider the other side of the transaction as discussed below. The government “loses” money It is highly likely that the government’s position is income neutral no matter when the deduction is available to the investor. When a property is negatively geared the gross income from the property doesn’t change, just the number of parties and the proportion in which the income is split. The interest payment is a cost to the investor, but it is income to the lender, and tax will be paid on it by the lender, their employees and depositors. Then there is the extra tax the government will reap through additional economic activity. Borrowings enable investors to purchase more rental properties than if they didn’t borrow. Some of these properties will be new builds. The government will gain revenue from the building activity including GST, payroll tax, company tax, and personal income tax. If investors borrow up to 80% of their purchases, this allows up to 4 more houses to be built than if they didn’t borrow. Forces home buyers out of the market One of the biggest furphies is that negative gearing gives a tax advantage to investors, allowing them to bid-up the price of houses. This is not true as home buyers are the most tax advantaged purchasers, and often also benefit from government schemes designed to get first home buyers into a house. The tax advantage occurs in two areas. On sale an investor has to pay capital gains tax, while a homeowner does not. Capital gains are generally the most significant income from real estate investments. Homeowners also get a tax benefit because they earn an imputed rent from their rental property on which they do not pay tax. This is balanced to some extent by not being able to tax deduct expenditure. All these factors mean that home buyers are more able to outbid investors than the other way around. That negative gearing plays a negligible role in restricting home ownership can be seen in the surge in home ownership after WWII from around 50% in 1950 to approximately 70% in 1970, during all of which time investment losses were deductible against other income. (See graph above).

Negative gearing increases house prices 70% of the price of a house is determined by interest rates. One reason house prices are currently so high is that we are at the end of the strongest decline in interest rates ever. Another reason is restrictions on housing supply through town planning schemes and regulations. A third is the upfront infrastructure charges levied against new home buyers. There is also a demand problem with Australia currently importing too many immigrants. Net inflows of 500,000 or so a year is more than the market can absorb, forcing prices (and rents) up. If we could increase supply and decrease the costs of development, then house prices would fall. The same would be true if we could reduce demand. If we abolish negative gearing, we know from the experience in 1985 that rents will increase because investors will withdraw from the market, leading to a decrease in housing starts, and potentially an increase in house prices. This is the last thing we need when there are not enough houses for the existing population, and there is a decrease in the numbers of potential home owners who can afford to purchase. For further information contact Graham Young on 0411 104 801 or graham.young@aip.asn.au

|